A trust fund isn’t just a tool for the ultra-wealthy; it’s a practical way for anyone to plan for their child’s future. It allows you to safeguard money, invest it, and ensure it’s used for specific purposes when your child needs it most.

But how much money you need to start a trust fund for a child? Is beginning with a small amount realistic, or does it require a six-figure fortune?

In this post, we’ll break down the costs, explore your options, and guide you through the process step by step. Whether planning for the short term or building a legacy for generations to come, you’ll discover that starting a trust fund is more attainable than you might think.

Contents

- 1 What is a Trust Fund?

- 2 How Much Money Do You Need to Start a Trust Fund?

- 3 Factors That Influence the Required Amount

- 4 Steps to Setting Up a Trust Fund

- 5 Benefits of Starting a Trust Fund Early

- 6 Common Misconceptions About Trust Funds

- 7 Tips for Making a Trust Fund Work for You

- 8 Maximize the Power of Your Trust Fund

What is a Trust Fund?

At its core, a trust fund is a financial tool that allows you to set aside money or assets for someone else’s benefit — typically your child. A trustee manages the funds and ensures the money or assets are used according to your instructions.

Unlike simple savings and investment accounts, trust funds offer greater control and protection over how and when the money is distributed. They can help pay for your child’s education, provide a down payment for their first home, or even be a safety net for unforeseen expenses.

There are different types of trust funds to consider:

- Revocable Trusts: These allow you to retain control and make changes during your lifetime.

- Irrevocable Trusts: These cannot be altered after being established, but they often come with tax advantages.

- Living Trusts: These are set up and take effect while you’re alive, ensuring your child has the financial support they need even in your absence.

By choosing the right type of trust fund, you can create a personalized plan that aligns with your goals and gives you peace of mind about your child’s future.

How Much Money Do You Need to Start a Trust Fund?

One of the biggest misconceptions about trust funds is that they require significant assets or a massive upfront investment.

The truth is, there’s no strict minimum. You can start a trust fund with as little or as much money as you’re comfortable contributing. What matters most is defining your goals and choosing the right type of trust to match them.

For example, some parents start with just $1,000 or even less and use the fund to teach their children about financial responsibility. Others might contribute tens or hundreds of thousands of dollars, particularly if the trust is designed for major expenses like college tuition or real estate.

It’s also important to factor in setup costs. While opening a simple trust may cost only a few hundred dollars, more complex trusts involving legal consultations and administrative services could require several thousand dollars.

Additionally, ongoing management fees may apply, especially if a professional trustee or financial advisor is involved.

The amount you start with is less important than having a clear plan for growing the fund over time. Regular contributions, whether monthly or annually, will help build a substantial nest egg for your child’s future without requiring a large initial investment.

Factors That Influence the Required Amount

The amount you need to start a trust fund depends on several factors, including your financial goals and the trust’s structure. Let’s break down the key considerations:

1. Goals of the Trust

Your trust fund’s purpose will heavily influence the required amount. For example: If the trust is meant to pay for your child’s college tuition, you might aim for $50,000 or more, depending on anticipated costs.

For a smaller goal, like providing a financial safety net, a few thousand dollars could be sufficient.

Clearly outlining your objectives will help you determine how much to contribute initially and over time.

2. Type of Trust

Different types of trusts have varying costs and funding requirements. A basic revocable trust may have minimal setup costs, while an irrevocable trust is designed for estate planning and tax benefits and might involve higher legal fees and initial funding amounts.

3. Ongoing Costs

Don’t forget about the ongoing expenses of maintaining a trust fund. These include:

- Trustee Fees: If you hire a professional trustee, expect to pay an annual percentage of the trust’s value.

- Legal and Administrative Fees: Attorneys and administrators charge for their services, which can vary based on the complexity of the trust.

- Asset Management Fees: If the funds are invested, a financial advisor or institution will charge fees for managing the trust assets.

4. State Laws and Tax Implications

The legal and tax environment in your state can also affect costs. For instance, some states have lower estate taxes on trust income, while others may require additional paperwork or fees to establish a trust.

Consider these factors upfront so you can plan more efficiently and set realistic expectations about the amount of money you’ll need to start and sustain your child’s trust fund.

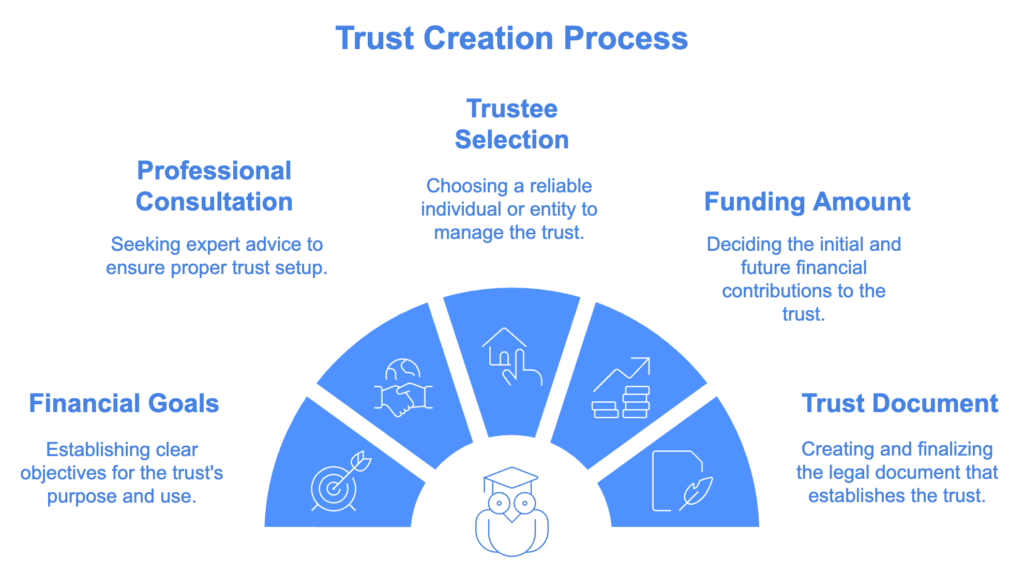

Steps to Setting Up a Trust Fund

Setting up a trust fund for your child may sound daunting, but it’s straightforward if you have the right information. Follow these steps to create a trust fund that fits your family’s needs and ensures your child’s financial future is secure:

Step 1: Define Your Financial Goals

Think about what you want the trust to accomplish. Is it for education? A safety net for unexpected expenses? Long-term wealth building? Clear goals will guide every decision you make during the setup process.

Step 2: Consult with a Professional

Work with a financial advisor or an estate planning attorney to determine the best type of trust for your needs. They’ll help you navigate legal requirements and create a plan that aligns with your financial situation.

Step 3: Choose a Trustee

Decide who will manage the trust. You can appoint family members, a trusted friend, or a professional trustee (such as a bank or law firm). Each option has pros and cons, so choose someone who will act in your child’s best interests and the trust.

Step 4: Determine the Initial Funding Amount

Decide how much money or assets you’ll contribute to the trust to get it started. Remember, you can always make additional contributions over time.

Step 5: Draft and Finalize the Trust Document

Your estate planning attorney will draft a legal document outlining the trust’s terms, including:

- Who the beneficiary is (your child)

- How and when the funds can be used

- Any specific instructions or restrictions

Review the document carefully and make sure it reflects your intentions before signing.

Step 6: Fund the Trust

Once the paperwork is complete, you’ll transfer assets into the trust. This can include cash, investments, property, or other valuable items.

Step 7: Make Future Contributions (Optional)

Trust funds don’t have to be one-and-done. Regular contributions, even small ones, can significantly grow the fund over time, especially if invested wisely.

Benefits of Starting a Trust Fund Early

Starting a trust fund for your child early comes with several significant advantages. Here’s why it pays to plan ahead:

- Compound Growth Over Time: When you start a trust fund early, the money has more time to grow through the power of compound interest. Even modest investments can snowball into substantial amounts if managed wisely. For example, starting with $5,000 and earning an average return of 6% annually could grow to over $15,000 in 20 years.

- Financial Security: Life is unpredictable, but a trust fund ensures your child has a safety net. Whether it’s for educational expenses, asset protection, medical emergencies, or other major milestones, having funds set aside provides peace of mind for both you and your child.

- Clear Boundaries for Fund Usage: Trust funds come with built-in rules. You decide how and when the money can be accessed — whether it’s tied to reaching a certain age, completing college, or other milestones. This ensures the funds are used responsibly and for their intended purpose.

- Possible Tax Advantages: Depending on the type of trust you set up, you could benefit from tax advantages. For example, an irrevocable trust may minimize estate taxes or shield assets from certain liabilities. Consult with a tax professional to explore the potential perks, including possible government benefits.

- Teaches Financial Responsibility: A trust fund isn’t just about providing money — it’s also an opportunity to teach your child about managing finances and assets wisely. By introducing them to the concept early, you’re setting them up for long-term financial literacy and success.

Ultimately, the earlier you start, the more time your contributions have to grow, and the greater the impact the trust can have on your child’s life. Even starting small can make a big difference in the long run.

Common Misconceptions About Trust Funds

Trust funds are often associated with many myths and misconceptions that can discourage parents from exploring this financial tool. Let’s debunk some of the most common untruths:

- Trust Funds Are Only for the Wealthy: Many people think trust funds are exclusive to multimillionaires, but that couldn’t be further from the truth. While wealthy families often use trusts for estate planning, anyone can set up a trust fund — even with modest contributions. It’s about protecting assets and planning for the future, not the size of your bank account.

- You Need a Huge Upfront Investment: Contrary to popular belief, you don’t need a fortune to start a trust fund. Some parents begin with as little as $1,000 or even less. Over time, regular contributions will help grow the fund into something substantial.

- Setting Up a Trust Fund Is Complicated: The process of creating a trust fund may seem intimidating, but it’s simpler than it looks. With the help of a financial advisor or estate planning attorney, you can set up a trust fund tailored to your needs without overwhelming trust documents or legal jargon.

- Trust Funds Are Too Rigid: Some parents worry that trust funds lock away money indefinitely, but that’s not true. You have control over how and when the funds are distributed. Whether you want to release funds at specific ages, for certain expenses, or in one lump sum, the terms are entirely up to you.

- Only Cash Can Be Put Into a Trust: Trusts can hold various assets beyond cash. You can include stocks, bonds, real estate, or other investments, allowing you to diversify and grow the trust fund more effectively.

Tips for Making a Trust Fund Work for You

A trust fund can be a powerful tool for your child’s financial future, but ultimately, how you manage it will make all the difference. Here are some practical tips to help you maximize its impact:

- Start Small and Build Over Time: Don’t feel pressured to contribute a large sum upfront. Begin with an amount that fits your budget and add to it regularly. Even small, consistent contributions can lead to significant growth over time, thanks to compound interest and smart investments.

- Choose the Right Trustee: Selecting the right trustee is crucial. If you opt for a family member, ensure they are trustworthy and financially savvy. If you choose a professional trustee, like an estate planning law firm, bank, or trust company, be mindful of the fees and services they provide.

- Monitor and Adjust: A trust fund isn’t a “set it and forget it” asset. Review its performance regularly and make adjustments as needed to ensure it aligns with your goals. Work with a financial advisor to optimize the trust’s investments.

- Educate Your Child: A trust fund is more than just a financial safety net — it’s an opportunity to teach your child about money management. As they grow older, involve them in conversations about the trust to help them understand its purpose and how to use it responsibly.

- Use Estate Planning Tools: Take advantage of modern tools and software that simplify trust management. These tools can help you track contributions, monitor growth, and stay organized.

Maximize the Power of Your Trust Fund

Establishing a trust fund for your child is a thoughtful and impactful way to secure their financial future. It’s a step that reflects careful planning and a commitment to their well-being.

While the process might seem daunting at first, understanding the basics and taking it one step at a time can make it manageable and rewarding. Remember, a trust fund is not just about accumulating wealth; it’s about providing security, teaching financial responsibility, and helping your child achieve their dreams.

By setting up a trust fund, you’re giving your child a gift that can last a lifetime, helping them navigate the financial challenges of adulthood with confidence and support.

Ready to explore more tips and strategies for smart financial planning?

Visit Money Saving Parent for actionable advice, resources, and expert insights to help you level up your family’s financial game. Your family’s financial future starts today — let’s make it count!