When it comes to building wealth, investing in stocks is often a go-to strategy. But what if your cash flow is tight and your credit card has some available balance? You might wonder, “Can I buy stocks with a credit card?” It sounds tempting, doesn’t it? A few clicks, a quick swipe, and you’re in the game.

The truth is, most major brokers don’t allow you to invest directly with a credit card, and those that do usually tack on extra fees or interest that can chip away at your returns faster than you might expect.

Today, we’ll break down everything you need to know about using your credit card to invest in stock options — from the practicalities and pitfalls to alternative ways you can fund your investments without taking on high-interest debt.

Keep reading to get a clear picture of whether using a credit card for investing is a smart move or a risk best left off the table.

Contents

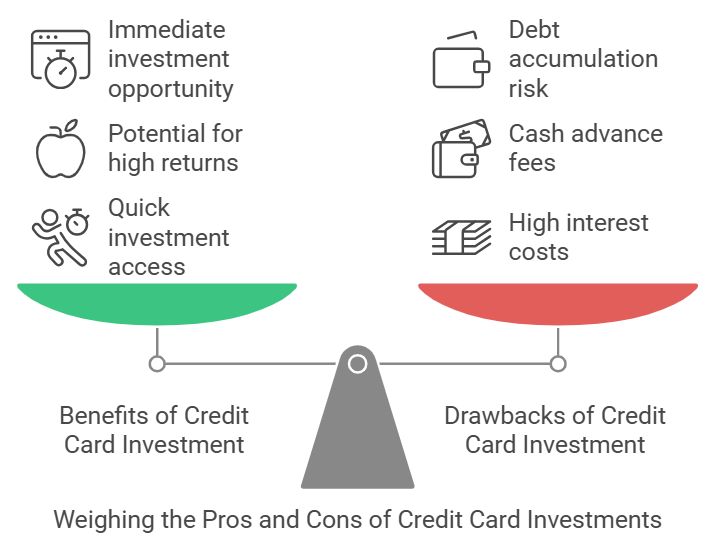

Can You Buy Stocks with a Credit Card?

If you’re eager to start building wealth through the stock market, it’s natural to think of using any available funds you have and that might include your credit card.

But can you actually use a credit card to buy stocks? The short answer is: not directly, at least not with most major brokerage platforms.

Why Most Brokers Don’t Allow It

The main reason you can’t buy stocks with a credit card through traditional brokers is that it’s considered too risky, both for the investor and the brokerage. Buying stocks comes with inherent risk, and adding credit card debt to the mix only magnifies those risks.

Most brokerage firms prefer responsible investing, which typically means funding your account with cash, not borrowed money that accrues interest.

Disallowing credit cards is actually a way of helping you avoid falling into a potential debt trap.

Possible Workarounds

While most brokers don’t offer a direct credit card funding option, some third-party financial services or peer-to-peer payment apps (like PayPal or Venmo) allow you to funnel money indirectly into buying stock.

However, these methods often treat the transaction as a “cash advance,” which can result in even higher fees and immediate interest charges.

For example, if you use a cash advance to transfer funds to a trading account, you could be charged advance fees that often range from 3% to 5% of the amount transferred, plus a higher-than-average APR.

So, while there might be some indirect routes to use a credit card to buy stock, they usually come with steep costs and aren’t considered best practices in the investing world.

Instead, explore safer and more direct methods, which we’ll cover in later sections.

Risks and Drawbacks of Buying Stocks with a Credit Card

Buying stocks with a credit card might seem like a quick way to get your investment journey started. In reality, it’s a high-risk, high-cost approach that could put your financial health in jeopardy.

There are some major risks and drawbacks that can turn this quick-fix investment into a financial setback. Here are the main reasons why funding your investments with a credit card might not be worth it in the long run:

1. High Interest Rates

Credit cards are notorious for their high interest rates, which often range between 15% to 25% (or higher, depending on your credit score and the type of card).

Unless your investment delivers immediate, high returns, which is extremely rare, you’re likely to pay more in interest than you could earn in stock gains. Even with a 0% APR promotional offer, any remaining balance after the promo period ends will start to accrue interest immediately.

In the long run, these interest fees can eat away at your investment returns, and you could lose money overall.

2. Cash Advance Fees

If you go through a third-party platform or workaround to use your credit card for stock purchases, you may incur advance fees.

These fees generally range from 3% to 5% of the transaction amount and start accruing interest immediately, often at a higher rate than regular purchases.

For example, if you transfer $5,000 to your trading account and face a 5% advance fee, that’s an instant $250 cost, even before you see any return on your investment.

3. Debt Accumulation and Financial Stress

Buying stocks with a credit card is essentially borrowing money to invest, and that debt has to be repaid, regardless of how your investments perform.

If the stock market fluctuates or your investment doesn’t perform as expected, you’ll still be on the hook for your credit card payments. Over time, carrying a balance on your card can snowball into overwhelming debt and potentially hurt your credit score if you miss any payments.

Eventually, what started as a simple investment could easily turn into financial stress, as credit card debt often grows faster than many realize.

4. Increased Risk of Loss

Investing in stocks always comes with a level of risk since there’s no guaranteed return. When you invest with a credit card, you’re increasing that risk by tying potential losses to a high-interest debt.

If your investment declines in value, not only will you lose money in the market, but you will also owe that amount plus additional credit card interest. It’s essentially a double loss: you’re out the invested money and face growing debt on the side.

5. Limited Returns Due to Fees and Interest

In investing, the goal is to maximize your returns by keeping costs low. Credit card fees, cash advance fees, and high interest rates make it incredibly difficult to see significant returns.

These extra costs add a lot of pressure on your investments to perform exceptionally well, which is unrealistic for most stock market investments, especially over short time frames.

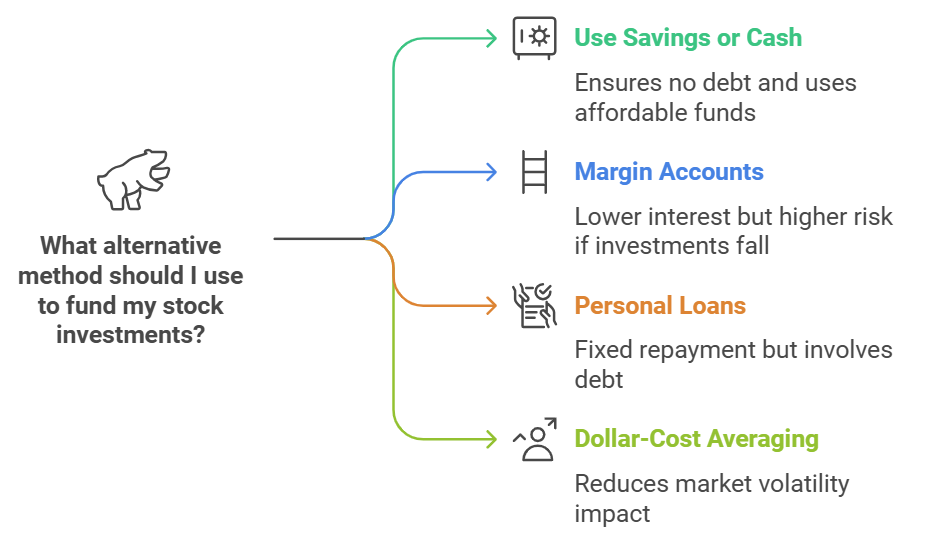

Alternatives to Buying Stocks with a Credit Card

If you’re interested in funding your stock investments but want to avoid the financial risks of using a credit card, there are safer and more cost-effective options to consider. These alternatives allow you to invest within your means and reduce the risk of accumulating high-interest debt.

1. Using Savings or Cash-on-Hand

The most straightforward and secure way to invest in stocks is to use cash or money from a dedicated savings account.

This approach keeps you from incurring debt and ensures you’re only investing money you can afford to lose. If you don’t have enough saved up, consider setting aside a portion of your income each month until you’ve built up enough to invest responsibly.

Investing with cash provides peace of mind, knowing you’re not risking borrowed funds, and any returns you make go directly toward growing your investment portfolio without being offset by interest payments.

2. Margin Accounts with Brokers

Many brokerage firms offer margin accounts that allow you to borrow money for investing, using your existing investments as collateral. While margin trading still involves borrowing money, the interest rates on margin loans are lower than those on credit cards.

However, margin accounts also come with their own risks. For example, if your investments lose value, you may face a margin call. This requires you to either deposit more funds into your investment account or sell off assets to cover the loss.

As such, using a margin account is best suited for experienced investors who understand the risks and can monitor their investments closely.

3. Personal Loans or Low-Interest Financing Options

If you’re comfortable with a little leverage but want to avoid high-interest credit card debt, consider a personal loan from a bank or credit union. These loans generally come with lower interest rates than credit cards, especially if you have a strong credit score.

A personal loan also provides a fixed repayment schedule, which can make budgeting easier and help you avoid the open-ended debt cycle that often comes with credit cards.

Keep in mind, however, that personal loans still involve debt. So, it’s essential to assess whether you’re in a stable enough financial position to take on this kind of commitment.

4. Dollar-Cost Averaging with Monthly Contributions

If you don’t have a large sum to invest all at once, consider using a strategy called dollar-cost averaging (DCA). With DCA, you invest a set amount at regular intervals, such as monthly, regardless of the stock’s price.

This approach helps reduce the impact of market volatility, as you’re buying shares at both high and low prices over time. Many investors prefer this method because it promotes consistency, reduces the need for a large initial investment, and limits risk by spreading out purchases.

5. High-Interest Savings Accounts or Emergency Funds

If you’re working on building up a stock investment fund, consider putting your money into a high-interest savings account. These accounts provide a modest return, which can help grow your investment savings while you wait for the right opportunity to enter the stock market.

Additionally, having an emergency fund ensures you’re financially stable enough to handle market fluctuations without needing to rely on credit or take on unnecessary risks.

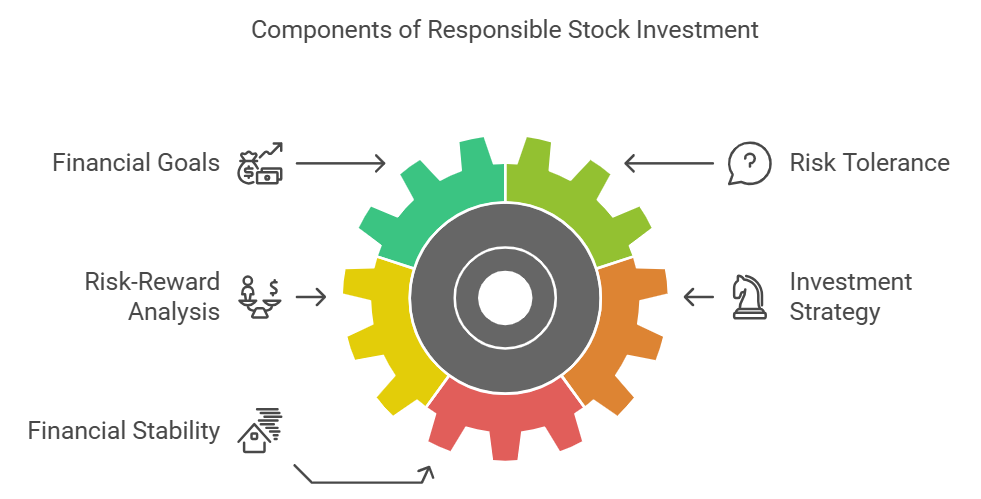

Tips and Considerations for Responsible Financial Management

Before deciding to fund your stock investments, whether by credit card or an alternative approach, it’s essential to think carefully about your financial situation and goals.

Here are some important factors to weigh to make the most informed choice possible.

Know Your Financial Goals and Risk Tolerance

Ask yourself what you’re hoping to achieve by investing in stocks. Are you looking for long-term growth, short-term gains, or perhaps a combination of both?

Knowing your financial goals will help you gauge whether taking on debt for an investment is worthwhile. Also, be honest about your risk tolerance. Stock investments can be volatile, and if using a credit card or loan would make you uncomfortable, it’s likely not the best choice for you.

Weigh Potential Risks Over Rewards

While the potential for high returns can make credit card funding tempting, remember that investing always carries risk. There’s no guaranteed profit in the stock market, and any downturn could leave you with both a financial loss and a lingering credit card debt to repay.

Consider whether the potential upside is worth the debt, fees, and financial stress that might come with a high-interest balance.

Be Realistic About Your Investment Strategy

Investing with borrowed money requires a very high return rate to cover the cost of interest and investment fees, especially when using credit cards.

Aiming for returns high enough to offset credit card interest may lead to risky investment choices or impatience when returns don’t materialize as quickly as hoped.

However, a steady, consistent approach using funds you already have is often more profitable and far less stressful in the long run.

Prioritize Financial Stability

Investing works best when you’re in a financially stable position. If you don’t have an emergency fund or you’re still working on reducing other debts, consider holding off on stock investments for now.

A solid financial foundation makes it easier to navigate market fluctuations without relying on credit, which can lead to much healthier long-term financial growth.

Conclusion

So, can you buy stocks with a credit card? Yes, but that’s a risk most of us just don’t need.

Between high interest rates, advance fees, and the potential for mounting debt, the downsides of funding investments with a credit card make it a bad idea and outweigh any potential benefits.

Instead, focus on investing with cash, leveraging lower-interest options, or building your portfolio slowly through dollar-cost averaging.

Remember, smart investing is about minimizing risks, maximizing gains, and protecting your financial health. Taking a steady, disciplined approach today will pay off big in the long run without the stress of high-interest debt hanging over you.

If you’re looking for more practical tips on managing your money and making savvy financial moves, check out our in-depth guides on Money Saving Parent for advice you can actually use.

Let’s make your financial goals a reality, one smart decision at a time!